Why understand CLO Structure?

Whether CFA, FRM, CA, or entry-level professionals— Most candidates preparing for roles in structured finance—have heard of terms like CLO structure, securitization, tranches, and waterfalls.

But very few can actually explain how a CLO works. (Read for what a CLO is…..)

Not because the concept is too complex…

But because it is often explained in a way that is too theoretical, fragmented, and disconnected from how these deals actually function in the real world.

Many candidates rely on textbooks or scattered online articles. They read definitions, memorize terms, and move on—without truly understanding how the entire structure fits together.

- They’ve read about tranches.

- They’ve heard about waterfalls.

- They’ve seen terms like OC test and IC test.

But when asked:

👉 “Explain how a CLO actually works…”

They freeze.

That’s where the problem begins.

Because in interviews—and more importantly, in real roles within trustees, collateral managers, or rating agencies—clarity matters more than definitions.

You need to understand:

→ How a CLO is built

→ Who is involved

→ How cash flows move

→ What happens when things go wrong

This guide is designed to bridge that gap.

It will break down CLO structure step-by-step, using simple language, practical insights, and real-world flow—so that you can not only understand the concept, but also explain it with confidence.

WHO THIS CLO STRUCTURE GUIDE IS FOR

Most candidates fail CLO interviews not because they don’t know the terms… but because they cannot explain the CLO structure simply.

This guide is designed for:

- CFA, FRM, CA, and finance students exploring structured finance

- Candidates preparing for roles in CLOs, securitization, or credit markets

- Entry-level professionals working with trustees, collateral managers, or rating agencies

- Anyone who understands the terminology—but wants to truly understand how CLOs work

- If you’ve ever felt that CLO concepts are clear in theory but confusing in practice, this guide is for you.

CLO STRUCTURE IN 60 SECONDS (SIMPLIFIED)

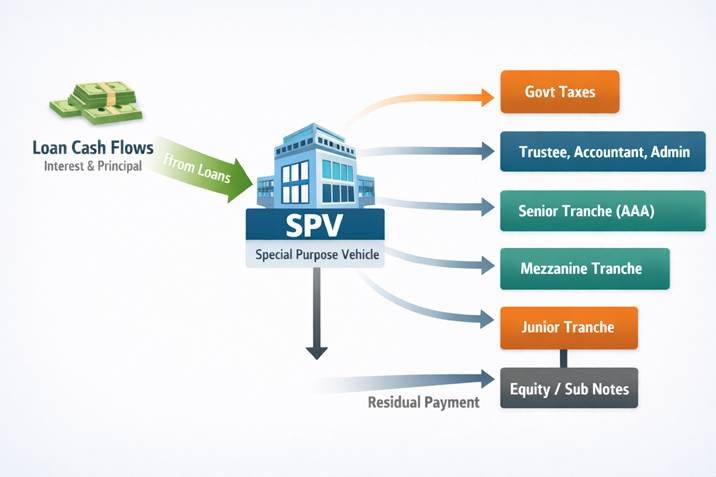

At its core, a Collateralized Loan Obligation (CLO) is a structured finance vehicle that pools together corporate loans and redistributes the cash flows to different investors.

Here’s the simplest way to think about it:

→ A pool of leveraged loans is created

→ These loans are transferred to a separate legal entity (SPV)

→ The SPV raises money by issuing different classes of securities (tranches)

→ Investors in these tranches receive payments based on a predefined priority

→ Cash flows from the loans are distributed through a waterfall

Each investor takes a different level of risk—and earns a different level of return—depending on where they sit in this structure.

CLO STRUCTURE

STEP 1: LOAN POOL CREATION

The foundation of any CLO is the underlying loan pool.

These are typically leveraged loans—loans extended to companies that already have a relatively high level of debt or lower credit ratings.

What are leveraged loans?

Issued to below-investment-grade companies

Offer higher yields to compensate for higher risk

Typically syndicated across multiple lenders

Who is involved in creating the loan pool?

Loan pool creation is not a single-entity process. It involves coordination between multiple participants:

Banks / arrangers → originate and structure loans

Institutional investors → participate in syndicated loans

CLO managers → select and accumulate loans for the portfolio

What does underwriting involve?

Underwriting includes:

- Assessing borrower credit quality

- Evaluating repayment capacity

- Structuring loan covenants

- Pricing risk appropriately

This stage is critical because:

The quality of the CLO depends heavily on the quality of its underlying loans

STEP 2: SPV FORMATION (ISSUER STRUCTURE)

Once the loan pool is identified, it is transferred to a Special Purpose Vehicle (SPV).

The SPV is the issuer of the CLO securities.

What is an SPV?

An SPV is a legally separate entity created solely for the purpose of holding assets and issuing securities.

Why is it called “bankruptcy remote”?

Because:

- The SPV is legally independent from the originating institution

- Its assets are isolated from the sponsor’s balance sheet

- If the sponsor goes bankrupt, the SPV remains unaffected

Why not issue bonds directly from the bank?

Instead of a bank issuing bonds:

- The SPV isolates risk

- Improves investor confidence

- Enables structured tranching

- Facilitates securitization

In simple terms:

SPV = Clean vehicle to package loans and distribute risk efficiently

STEP 3: TRANCHING (SUBORDINATION STRUCTURE)

Once the SPV is set up, it raises capital by issuing different classes of securities, known as tranches.

Each tranche has:

Different risk levels

Different return expectations

Different payment priority

Typical CLO Tranches (more on CLO structures…)

| Tranche | Risk Level | Return | Payment Priority |

| Senior (AAA) | Lowest | Lowest | Paid first |

| Mezzanine | Medium | Medium | Paid after senior |

| Equity | Highest | Highest | Paid last |

How does this structure work?

This is called subordination:

- Losses are absorbed from bottom (equity) upward

- Payments are made from top (senior) downward

Why is this important?

This structure:

- Protects senior investors

- Attracts different investor types

- Enables risk redistribution

In simple terms:

Tranching = Dividing risk and return across investors

STEP 4: CAPITAL RAISING (FUNDING THE CLO)

Once the SPV is structured and tranches are defined, the next step is raising capital from investors.

The SPV issues notes (bonds) corresponding to each tranche and offers them to institutional investors.

Who invests?

- Insurance companies → Senior tranches (AAA)

- Asset managers → Mezzanine tranches

- Hedge funds / private equity → Equity tranche

How are these securities sold?

- Through investment banks / arrangers

- Via private placements (not retail)

Based on:

- Credit rating

- Yield

- Risk profile

What determines investor interest?

- Quality of underlying loan pool

- CLO manager track record

- Structure of tranches

- Market conditions

👉 In simple terms:

CLO raises money by selling different risk-return slices to different investors

STEP 5: CLO DEAL CLOSING & EFFECTIVE DATE

CONTENT

After capital is raised, the CLO transaction moves toward closing.

What happens at closing?

Legal documentation is finalized

Notes are issued to investors

Funds are transferred to the SPV

Initial loan portfolio is acquired

What is the “Effective Date”?

The effective date is when:

The CLO meets all required conditions

Portfolio composition satisfies eligibility criteria

Ratings are confirmed by rating agencies

If conditions are NOT met:

The deal may fail

Or require restructuring

Why is this stage important?

Because this is where:

The CLO officially becomes operational

STEP 6: PORTFOLIO MANAGEMENT (ACTIVE MANAGEMENT)

CONTENT

Unlike many securitized products, CLOs are actively managed.

What does this mean?

The CLO manager continuously manages the portfolio:

- Buying new loans

- Selling underperforming loans

- Optimizing yield and risk

Why is this important?

Because:

- The loan pool is dynamic, not static

- Performance depends on manager decisions

Key objective of the manager:

Maximize returns for equity investors while maintaining compliance with:

- OC tests

- IC tests

- Portfolio constraints

In simple terms:

CLO = actively managed loan portfolio, not a fixed pool

STEP 7: CASH FLOW GENERATION IN CLO STRUCTURE

CONTENT

Once the portfolio is active, the CLO starts generating cash flows.

Source of cash flows:

Interest payments from loans

Principal repayments

Prepayments

Recoveries (in case of defaults)

Two types of cash flows:

- Interest proceeds

- Principal proceeds

Why distinction matters?

Because:

- Interest → used for payments (fees, coupons)

- Principal → used for reinvestment or debt repayment

In simple terms:

Loans generate cash → CLO redistributes it

STEP 8: WATERFALL EXECUTION (CORE STRUCTURE MECHANISM)

CONTENT

This is the heart of a CLO.

The waterfall defines how cash is distributed. (Find More on CLO Waterfall…)

Two types of waterfall:

- Interest waterfall (Priority of Interest – POI)

- Principal waterfall (Priority of Principal – POP)

Typical order of payments:

- Fees (trustee, manager)

- Senior tranche interest

- Mezzanine tranche interest

- Principal payments

- Equity (residual cash)

What happens if tests fail?

If OC/IC tests fail:

- Cash is diverted away from junior tranches

- Used to repay senior debt

This is called:

Cash flow diversion mechanism

Why this matters?

Because:

Waterfall determines who gets paid—and who doesn’t

STEP 9: OC / IC MONITORING & EQUITY DISTRIBUTION

CONTENT

To protect investors, CLOs use coverage tests.

OC Test (Overcollateralization)

Measures:

👉 Asset value vs debt

Formula (conceptual):

OC = Total collateral / Total debt

Meaning:

Higher OC → safer structure

Lower OC → higher risk

IC Test (Interest Coverage)

Measures:

Ability to service interest payments

Meaning:

Ensures enough income is generated

Protects senior investors

What happens when IC/OC tests fail?

- Cash is diverted

- Junior tranches stop receiving payments

- Senior debt gets priority

This ensures:

Investor protection through structural safeguards

Equity Distribution

After all obligations are met:

Remaining cash goes to:

Equity investors

Key point:

- Highest risk

- Highest potential return

In simple terms:

Equity = residual claimant of CLO cash flows

→ “Detailed CLO Tranches Guide”

CLO Structure – Tranches Explained (AAA to Equity)

A key component of any CLO structure is how it divides risk and return across different investors. This is achieved through tranching, where the CLO issues multiple layers of securities, each with a different level of risk, return, and payment priority.

Understanding tranches in CLO Structure is essential to understanding how the overall CLO structure works in practice.

What are CLO Tranches in a CLO Structure?

In a typical CLO structure, the capital raised by the SPV is split into different tranches:

Senior tranches (AAA-rated)

Mezzanine tranches (AA to BB)

Equity tranche (unrated)

Each tranche has a specific position in the cash flow waterfall, which determines when and how it gets paid.

Typical CLO Structure – Tranche Hierarchy

| Tranche Type | Rating | Risk Level | Return | Payment Priority |

| Senior | AAA | Lowest | Lowest | First |

| Mezzanine | AA–BB | Medium | Medium | After senior |

| Equity | Not rated | Highest | Highest | Last |

How Risk and Return Work in a CLO Structure

The CLO structure is built on a simple principle:

Lower risk → Lower return

Higher risk → Higher return

Senior (AAA) Tranches

Get paid first in the waterfall

Protected by subordination

Lowest risk

Lowest yield

These investors rely on the strength of the CLO structure and coverage tests for protection.

Mezzanine Tranches

Paid after senior tranches

Moderate risk exposure

Higher return than senior

Their performance depends on both asset quality and structural protection within the CLO.

Equity Tranche

Paid last (residual cash flows)

No guaranteed payments

Highest risk

Potentially highest return

Equity investors benefit when the CLO structure performs well, but are the first to absorb losses.

Why Tranching is Critical to CLO Structure

Tranching is what makes a CLO structure viable and attractive to different types of investors.

It allows:

- Conservative investors → to invest in low-risk senior tranches

- Yield-seeking investors → to invest in mezzanine tranches

- Risk-tolerant investors → to invest in equity

In simple terms:

CLO structure works because risk is redistributed across tranches

Key Insight (For Interview + Real-World Edge)

Many candidates can list tranches…

But struggle to explain how they connect to the CLO structure.

- The correct way to think about it:

- Tranches define who takes risk

- Waterfall defines who gets paid first

- OC/IC tests define who gets protected

If you can connect these three, you understand how a CLO structure actually works—not just in theory, but in real deals.

CLO Structure – Waterfall Explained (Payment Priority with Example)

A critical part of any CLO structure is the waterfall mechanism, which determines how cash flows are distributed among different stakeholders.

It answers one simple but powerful question:

Who gets paid first—and who gets paid last?

What is the Waterfall in a CLO Structure?

In a CLO structure, cash generated from the underlying loan pool does not go to all investors equally.

Instead, it flows in a strict priority sequence, known as the waterfall.

In simple terms:

Cash flows from top to bottom

Losses are absorbed from bottom to top

CLO Structure – Payment Priority (Step-by-Step)

Let’s break the CLO waterfall into numbered steps for clarity:

1. Fees & Administrative Expenses

- Trustee fees

- CLO manager fees

- Legal and administrative costs

These are always paid first in the CLO structure

2. Senior Tranche Interest (AAA)

- Interest payments to senior noteholders

- Lowest risk investors

- Highest priority among investors

3. Mezzanine Tranche Interest

- Paid after senior tranches

- Includes AA, A, BBB, BB rated tranches

4. Principal Payments / Debt Repayment

- Used to pay down senior or mezzanine debt

- Or reinvest (depending on deal stage)

5. Junior / Subordinated Payments

- Lower-rated tranches receive payments

- Higher risk exposure

6. Equity Distribution (Residual Cash)

- Whatever cash remains goes to equity investors

- This is the last step in the CLO structure

Visual Flow (Use this for your diagram slide)

Loan Cash Flows

↓

[1] Fees

↓

[2] Senior (AAA)

↓

[3] Mezzanine

↓

[4] Principal / Reinvestment

↓

[5] Junior Tranches

↓

[6] Equity (Residual)

Numerical Example (MOST IMPORTANT SECTION)

Let’s say the CLO generates:

$100 of cash flow

Step-by-step distribution:

Fees → $5

Senior interest → $50

Mezzanine interest → $20

Principal repayment → $10

Junior tranches → $5

Equity → $10

Now imagine cash flow drops to $70:

Fees → $5

Senior → $50

Mezzanine → $15

Others → $0

Equity gets nothing.

What Happens During Stress (Critical Insight)

In a stressed scenario within a CLO structure:

Lower tranches lose income first

Equity gets wiped out first

Senior investors remain protected

This is why:

CLO structure is designed to protect senior investors through payment priority

Why This Matters (Interview + Real World)

Most candidates say:

❌ “Waterfall is payment order”

Top candidates say:

✅ “Waterfall defines risk transfer through cash flow priority in a CLO structure”

That’s the difference between:

Memorization

Understanding

Key Takeaway

CLO structure works because of the waterfall

Waterfall determines survival of each tranche

→ “CLO Waterfall Explained (Full Guide)”

CLO Structure – OC & IC Tests Explained (What, Why, and Impact with Example)

A critical protection layer within any CLO structure is the use of coverage tests—specifically the Overcollateralization (OC) Test and the Interest Coverage (IC) Test.

These tests ensure that the CLO structure remains stable, even when the underlying loan portfolio starts to deteriorate.

What are OC & IC Tests in a CLO Structure?

👉1. Overcollateralization (OC) Test (more on OC Test….)

The OC test measures whether the value of assets is sufficient compared to the debt issued.

📊 Formula (Conceptual):

OC Ratio = Total Collateral Value / Total Debt Outstanding

👉 Example:

Total loan pool = $120 million

Total debt issued = $100 million

OC Ratio = 120 / 100 = 1.20x

👉 This means the CLO structure has 20% extra collateral as protection

👉 2. Interest Coverage (IC) Test

The IC test checks whether the CLO generates enough income to pay interest obligations.

📊 Formula (Conceptual):

IC Ratio = Interest from Assets / Interest Paid to Debt Investors

👉 Example:

Interest income = $12 million

Interest payable = $10 million

IC Ratio = 12 / 10 = 1.20x

👉 This means the CLO structure comfortably covers interest payments

Why OC & IC Tests are Important in a CLO Structure

These tests are not just calculations—they are control mechanisms.

They ensure:

- Senior investors are protected

- Cash flows are monitored continuously

- Risk is actively managed

👉 In simple terms:

OC = Asset protection

IC = Income protection

Impact of OC & IC Test Failure (MOST IMPORTANT)

This is where theory meets reality.

📉 Scenario: OC Test Failure

Let’s say:

Collateral drops to $105 million

Debt remains $100 million

OC Ratio = 105 / 100 = 1.05x

👉 Required threshold = 1.20x

👉 Test FAILS ❌

What happens next in the CLO structure?

- Cash flow changes immediately at the next payment date:

- Equity receives $0

- Junior tranches receive reduced or no payments

- Cash is diverted to repay senior debt

👉 This is called:

Cash flow diversion mechanism

Scenario: IC Test Failure

Let’s say:

Interest income falls to $9 million

Interest payable remains $10 million

IC Ratio = 9 / 10 = 0.90x

👉 Required threshold = 1.10x–1.20x

👉 Test FAILS ❌

🔥 Impact:

Interest payments to junior tranches are cut

Cash is redirected to senior investors

Equity receives nothing

Combined Impact on CLO Structure

When OC or IC tests fail:

Waterfall priority changes

Cash flow gets redirected

Risk shifts upward

👉 This ensures:

Senior tranches remain protected

Structure remains stable

Key Insight (Interview + Practical Edge)

Most candidates say:

❌ “OC and IC are ratios”

Top candidates say:

✅ “OC and IC tests dynamically control cash flow distribution within the CLO structure”

Final Takeaway

OC and IC tests are the backbone of risk control in a CLO structure

They determine how stress is absorbed across tranches

→ OC Test article

→ IC Test article

CLO Structure – Distribution Waterfall (Tabular Example)

This table shows how cash flows are distributed in a CLO structure under a simplified interest waterfall scenario.

🔽 Interest Waterfall (Priority of Interest – POI)

📊 Assumption:

👉 Total Interest Proceeds = $10,000,000

🧾Sample Clo Structure Waterfall Distribution Table

| Step | Item | Available Amount ($) | Optimal Amount ($) | Paid Amount ($) | Running Balance ($) |

| 1 | Govt Taxes | 10,000,000 | 200,000 | 200,000 | 9,800,000 |

| 2 | Accountant’s Fee | 9,800,000 | 100,000 | 100,000 | 9,700,000 |

| 3 | Trustee Fee | 9,700,000 | 150,000 | 150,000 | 9,550,000 |

| 4 | Senior Management Fee | 9,550,000 | 250,000 | 250,000 | 9,300,000 |

| 5 | Senior Tranche Interest | 9,300,000 | 6,000,000 | 6,000,000 | 3,300,000 |

| 6 | Mezzanine Interest | 3,300,000 | 2,000,000 | 2,000,000 | 1,300,000 |

| 7 | Junior / Sub Notes | 1,300,000 | 800,000 | 800,000 | 500,000 |

| 8 | Equity Distribution | 500,000 | Residual | 500,000 | 0 |

👉 Key Insight:

Each step in the CLO structure gets paid only if sufficient cash is available

🔽 Principal Waterfall (Reinvestment Phase)

📊 Assumption:

👉 Total Principal Proceeds = $5,000,000

🧾 Distribution Table

| Step | Item | Available Amount ($) | Optimal Amount ($) | Used Amount ($) | Running Balance ($) |

| 1 | Reinvestment in New Loans | 5,000,000 | 4,500,000 | 4,500,000 | 500,000 |

👉 Key Insight:

In the CLO structure, principal is typically reinvested before being distributed

⚠️ Stress Scenario Insight (Optional Add-on Table)

If interest reduces to $7,000,000:

Fees still paid

Senior still protected

Mezz may be partially paid

Equity = $0

👉 This reinforces:

CLO structure prioritizes stability by protecting senior tranches first

⚠️ Practical Insight (Important)

Even though equity is not shown in this POI table:

Equity only receives cash after all above steps are fully satisfied

In stressed scenarios, equity often receives $0

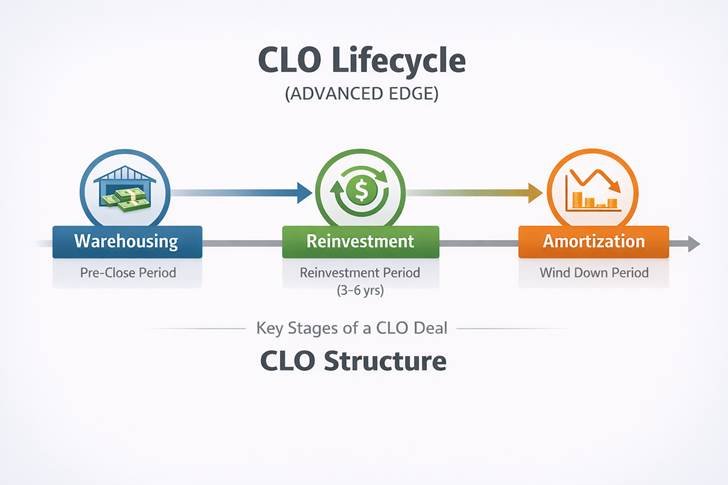

CLO Structure – Lifecycle Explained (Warehousing → Reinvestment → Amortization)

Understanding the CLO structure lifecycle is what separates:

👉 Basic learners

from

👉 Real structured finance professionals

A CLO is not static — it evolves through distinct phases over time.

🧩 Example CLO Deal Timeline

Let’s assume a CLO deal with the following structure:

Deal Launch Date: Jan 1, 2025

Reinvestment Period: 4 years

Legal Maturity: 10 years

🔹 Phase 1: Warehousing Period (Pre-CLO Formation)

📅 Timeline: Jul 2024 → Dec 2024

👉 What happens here?

Before the CLO is issued, the collateral manager starts accumulating loans.

Loans are purchased gradually

Funded through a warehouse line (bank financing)

Portfolio is built in advance

💰 Example:

Loans accumulated: $120 million

Funded by warehouse lender: $100 million

Equity contribution: $20 million

👉 This stage is critical because:

Quality of assets selected here defines future CLO performance

🔹 Phase 2: CLO Closing (Day 1 of CLO Structure)

📅 Date: Jan 1, 2025

👉 What happens in CLO Closing Date?

- SPV is formed

- Notes are issued (AAA → Equity)

- Warehouse loan is repaid

- Portfolio is transferred into the CLO

💰 Example:

CLO issues: $100 million debt + $20 million equity

Warehouse lender gets repaid

CLO structure officially begins

🔹 Phase 3: Reinvestment Period (Active Management Phase)

📅 Timeline: Jan 2025 → Dec 2028

👉 What happens in Reinvestment Phase?

This is the most dynamic phase of the CLO structure:

Principal proceeds are reinvested

Manager actively buys/sells loans

Portfolio is optimized for yield

💰 Example Cash Flow:

Annual principal repayments: $10 million

Instead of paying investors → reinvested into new loans

👉 Why this matters:

Reinvestment keeps the CLO structure alive and income-generating

🔹 Phase 4: End of Reinvestment (Transition Phase)

📅 Date: Dec 2028

👉 What changes after Reinvestment Phase?

- Reinvestment stops

- No new loans purchased

- Focus shifts to deleveraging the structure

🔹 Phase 5: Amortization Period (Wind-Down Phase)

📅 Timeline: Jan 2029 → Dec 2034

👉 What happens during Amortization Phase?

Now the CLO structure starts paying down debt:

Principal proceeds are used to repay tranches

Senior tranches get paid first

Risk reduces over time

💰 Example:

Annual principal: $10 million

Used to repay:

AAA → first

Then mezzanine

Then junior

👉 Key structural shift:

From reinvestment → to debt repayment

🔹 Phase 6: Final Maturity (End of CLO Structure)

📅 Date: Dec 2034

👉 What happens on Maturity?

- All debt tranches repaid

- Remaining cash goes to equity

- CLO structure terminates

FULL CLO STRUCTURE TIMELINE SUMMARY

Warehousing → CLO Closing → Reinvestment → Amortization → Maturity

🎯 Key Insight (Interview Edge)

Most candidates say:

❌ “CLO has reinvestment period”

Top candidates say:

✅ “CLO structure transitions from capital deployment to capital recovery over its lifecycle”

CLO Structure – Real-World Insights (Monthly vs Payment Period & OC Failure)

Understanding the CLO structure goes beyond theory.

What truly differentiates professionals is knowing how things work in real operations.

📅 Monthly vs Payment Period in a CLO Structure

In a typical CLO structure, there are two parallel timelines:

👉 Monthly reporting cycle

👉 Quarterly (or semi-annual) payment cycle

🔹 Monthly (Ongoing Monitoring)

Collateral data is updated every month

Key metrics tracked:

- Portfolio balance

- Defaulted assets

- WARF (credit quality)

- OC/IC ratios

👉 Example:

Jan month-end report shows:

OC Ratio = 122% (passing)

Loan defaults increased slightly

🔹 Payment Period (Actual Cash Movement)

Happens typically every 3 months

Determines:

- Who gets paid

- Whether tests are passing or failing

- Whether cash diversion happens

👉 Example:

March payment date:

OC Ratio drops to 118% (below 120% trigger)

Now the CLO structure reacts

👉 Key Insight:

Monthly reports show signals. Payment dates trigger actions.

⚠️ What Happens When OC Test Fails in a CLO Structure

The Overcollateralization (OC) test is one of the most critical protections in a CLO structure.

It measures:

👉 Assets available vs debt outstanding

🔹 Example Scenario

Total Loan Portfolio = $120 million

Debt Outstanding = $100 million

OC Ratio = 120% (threshold)

❌ Now, Stress Happens

Loan defaults increase

Portfolio value drops to $115 million

👉 New OC Ratio:

= 115 / 100 = 115% (FAIL)

🔄 Immediate Impact in CLO Structure

Once OC fails:

❌ Payments to junior tranches stop

❌ Equity receives $0

🔁 Cash is diverted

✅ Extra cash used to repay senior debt

💡 Real Operational Impact

Analysts must track OC breaches in reports

Trustees execute cash diversion

Portfolio managers may sell/buy loans to cure the breach

👉 Key Insight:

OC failure converts the CLO structure from yield distribution mode to capital protection mode

🎯 Why this matters

Most candidates explain:

❌ “OC test protects investors”

Top candidates explain:

✅ “When OC fails, the CLO structure dynamically redirects cash from equity to senior debt repayment”

This is the level of clarity that gets you hired.

CLO Structure – Interview Questions & How to Answer

Most candidates know terms.

Very few can explain the CLO structure clearly.

Here are high-impact interview questions — and how to answer them.

❓ 1. What is a CLO structure?

👉 How to answer:

A CLO structure is a securitization framework where a pool of leveraged loans is packaged into an SPV, which issues different tranches of debt and equity. Cash flows from the loans are distributed through a waterfall based on priority.

❓ 2. How does cash flow work in a CLO structure?

👉 How to answer:

Cash flows (interest + principal) from loans enter the SPV and are distributed sequentially—fees first, then senior tranches, followed by mezzanine and junior tranches, with residual going to equity.

❓ 3. Who gets paid first in a CLO structure?

👉 How to answer:

Payments follow strict priority: expenses and fees → senior debt (AAA) → mezzanine → junior → equity (last).

❓ 4. What happens during reinvestment period?

👉 How to answer:

During reinvestment, principal proceeds are used to purchase new loans instead of repaying investors, helping maintain portfolio size and yield.

❓ 5. What are OC and IC tests in CLO structure?

👉 How to answer:

OC (Overcollateralization) and IC (Interest Coverage) tests ensure sufficient asset coverage and cash flow. If breached, cash is diverted from junior tranches to repay senior debt.

❓ 6. Why is SPV used in CLO structure?

👉 How to answer:

The SPV isolates assets from the originator, making the structure bankruptcy-remote and protecting investors.

❓ 7. Why is CLO called actively managed?

👉 How to answer:

Because the manager actively buys and sells loans during the reinvestment period to optimize returns.

👉 Positioning line:

If you can explain CLO structure like this, you’re already ahead of most candidates.

FAQ – CLO Structure

What is CLO structure?

A CLO structure is a securitization mechanism where corporate loans are pooled and financed through multiple tranches with different risk-return profiles.

How does CLO structure work?

Loans generate cash flows, which flow into an SPV and are distributed through a predefined waterfall to investors based on priority.

Who gets paid first in a CLO structure?

Fees and senior tranche investors are paid first, while equity investors receive residual cash after all obligations are met.

Conclusion – CLO Structure Simplified

Understanding the CLO structure is not about memorizing terms.

It’s about understanding:

✔ How cash flows

✔ Who gets paid

✔ How risk is structured

Most people stop at theory.

Very few understand how it actually works.

If you’re serious about breaking into structured finance:

Start thinking in cash flows, not concepts

Focus on real deal mechanics

Practice explaining the CLO structure simply