Why Many Finance Professionals Hear About OC Tests But Don’t Fully Understand Them

Many professionals working in structured finance hear the phrase “OC test failed” or “OC trigger breached” during CLO reporting discussions.

But when asked what the OC test actually measures, many struggle to explain it clearly.

In real CLO deals, the Overcollateralization (OC) Test is one of the most important risk protection mechanisms for investors.

It directly affects:

- Cash flow distribution

- Waterfall priorities

- Equity payments

- Debt protection

For analysts working in CLO middle office, trustee reporting, or deal compliance, understanding the OC test is essential.

This article provides a clear, practical explanation of the CLO overcollateralization test, including how it works, why it matters, and how it appears in real workflows.

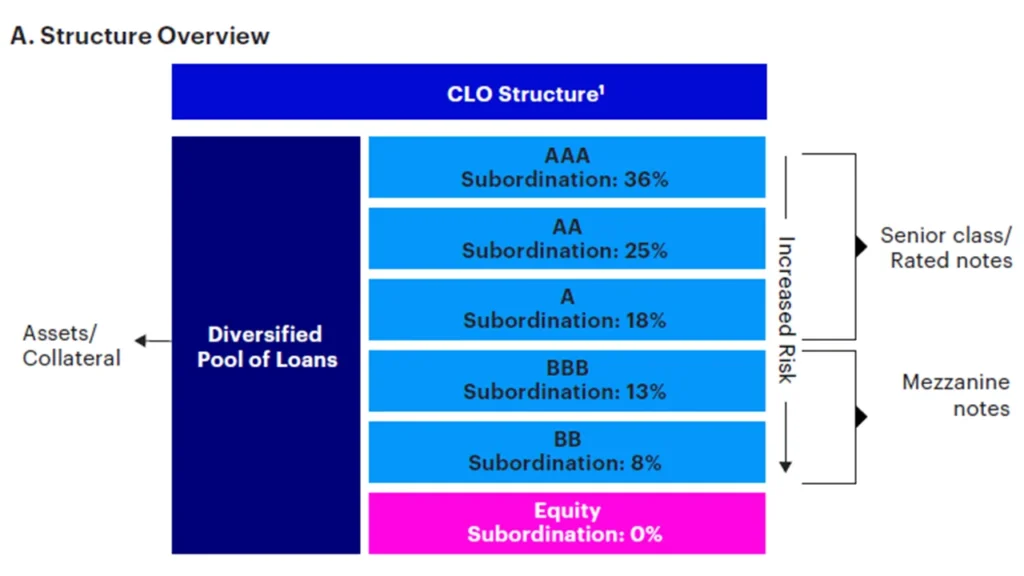

What Is the Overcollateralization Test in a CLO?

The Overcollateralization (OC) Test is a coverage test used in CLO deals to ensure that the collateral portfolio value is sufficient to support the issued debt tranches.

In simple terms:

It checks whether the CLO has enough loan collateral compared to the debt issued to investors.

Think of it like a safety cushion.

If a CLO has:

- $500 million in loans

- $400 million in debt issued to investors

Then the structure has extra collateral protecting lenders.

The OC test measures this relationship using the OC ratio.

When the ratio falls below a predefined threshold, the OC trigger is breached, and the deal enters cash flow diversion mode.

This protects senior investors.

CLO OC Ratio Meaning

The OC ratio compares the value of collateral assets with the outstanding balance of debt tranches.

Conceptually:

OC Ratio = Collateral Value ÷ Debt Outstanding

Each debt tranche has its own OC test.

Typical examples include:

| Tranche | OC Test |

|---|---|

| Class A | Senior OC Test |

| Class B | Mezzanine OC Test |

| Class C | Junior OC Test |

Senior tranches typically require higher protection levels.

Example threshold:

| Tranche | Required OC Ratio |

|---|---|

| Class A | 130% |

| Class B | 120% |

| Class C | 110% |

If the calculated ratio falls below the trigger, the test fails.

How the OC Test Works in a CLO (Step-by-Step)

Let’s break down the OC test in CLO deals in practical steps.

Step 1: Calculate Adjusted Collateral Value

The CLO administrator calculates the adjusted principal balance of the loan portfolio.

Adjustments may include:

- Defaulted loan haircuts

- CCC excess haircuts

- Recovery assumptions

- Market value adjustments (in some deals)

This gives the effective collateral value.

Step 2: Identify Debt Outstanding

Next, the outstanding balances of CLO debt tranches are determined.

Example:

| Tranche | Outstanding Balance |

|---|---|

| Class A | $300M |

| Class B | $60M |

| Class C | $40M |

Each tranche will have a separate OC test calculation.

Step 3: Calculate the OC Ratio

For each tranche:

Collateral Value ÷ Debt Outstanding

Example for Class A:

Collateral = $500M

Debt = $300M

OC Ratio = 166.7%

Step 4: Compare With Trigger Level

If the required Class A OC trigger = 130%

Then:

166.7% > 130%

Result:

Test passes.

Step 5: Monitor Monthly

CLO deals typically run monthly coverage tests.

These results appear in:

- Trustee reports

- Investor reports

- Compliance reports

CLO OC Test Example (Practical Scenario)

Let’s walk through a simple CLO OC test example.

CLO Structure

Collateral Loans = $500M

Debt Issued:

| Tranche | Balance |

|---|---|

| Class A | $320M |

| Class B | $60M |

| Class C | $40M |

Total Debt = $420M

Calculate Class A OC Ratio

OC Ratio = Collateral / Class A Debt

= 500 / 320

= 156%

If the trigger = 130%

Result → Pass

Now Assume Loan Defaults Occur

Collateral drops to $380M

New OC ratio:

380 / 320

= 118.75%

Now:

118.75% < 130%

This means the Class A OC trigger is breached.

What Happens When the OC Test Fails?

When a CLO OC trigger is breached, the waterfall changes.

Instead of paying equity investors, cash flows are redirected to repay senior debt.

This is called:

Cash flow diversion.

New waterfall priority becomes:

- Senior expenses

- Senior management fees

- Pay down senior notes

- Cure OC test

- Only then pay equity

This mechanism protects senior investors from collateral deterioration.

Where the OC Test Appears in Real CLO Workflows

Understanding the CLO overcollateralization test explained becomes critical in day-to-day structured finance work.

Trustee Reporting Teams

Trustees calculate coverage tests in monthly reports.

Tasks include:

- Calculating OC ratios

- Checking triggers

- Reporting pass/fail status

CLO Middle Office Teams

Investment bank teams monitor:

- Deal compliance

- Test breaches

- Portfolio quality

They often track OC cushion levels.

Collateral Managers

Managers actively manage the loan portfolio to ensure:

- OC tests remain compliant

- Collateral value stays strong

They may trade loans to maintain coverage.

Investor Reporting

Investors closely watch:

- OC ratios

- Trigger breaches

- Structural protections

These metrics determine deal health.

Where You See OC Tests in Deal Documents

OC tests appear in several operational reports:

| Document | Purpose |

|---|---|

| Trustee Reports | Coverage calculations |

| Monthly Investor Reports | Deal performance |

| Compliance Certificates | Test results |

| Waterfall Models | Cash flow allocation |

| Surveillance Reports | Risk monitoring |

Analysts working in structured finance operations frequently interact with these reports.

Common Mistakes Beginners Make About OC Tests

Many beginners misunderstand the OC test in CLO structures.

Here are common misconceptions.

1. OC Test Is Not a Market Price Test

It is based on adjusted principal balances, not daily market values.

2. OC Tests Are Different From Interest Coverage Tests

CLO deals typically include two major tests:

- OC Test (Collateral Protection)

- IC Test (Interest Protection)

Both serve different purposes.

3. OC Test Failures Do Not Mean Immediate Default

A breach simply triggers cash diversion.

The deal may still recover.

4. Every Tranche Has Its Own Test

Each tranche level has different:

- triggers

- protection levels

- coverage requirements

Why This Concept Matters in CLO Jobs

Understanding clo coverage tests explained is critical for professionals working in:

Investment Banks

Teams monitoring structured credit portfolios need to track:

- coverage ratios

- deal compliance

- trigger risks

CLO Administrators

Administrators calculate:

- coverage tests

- compliance metrics

- waterfall allocations

Trustees

Trustees verify whether deals are structurally compliant.

Consulting Firms

Firms like Deloitte or EY often support:

- structured finance reporting

- securitization analytics

- deal monitoring

Knowledge of OC tests is expected in interviews and daily work.

Career Insight: Why Analysts Must Understand the OC Test

For anyone pursuing a career in structured finance or CLO reporting, this concept is fundamental.

Interviewers often ask:

- What is the OC test in CLO?

- What happens when the OC test fails?

- How does it affect the waterfall?

Understanding the OC test helps analysts:

- interpret trustee reports

- understand deal health

- perform compliance monitoring

- build CLO waterfall models

It also signals that the candidate understands real deal mechanics, not just theory.

Quick Summary

Here are the key takeaways.

• The OC test ensures CLO collateral is sufficient to support debt tranches.

• It compares collateral value to outstanding debt.

• Each tranche has its own OC trigger level.

• If the ratio falls below the trigger, the OC test fails.

• A failure triggers cash flow diversion to repay senior debt.

• OC tests are calculated monthly in trustee reports.

• They are critical for deal protection and investor confidence.

FAQ: CLO Overcollateralization Test Explained

What is the OC test in CLO?

The OC test measures whether the value of CLO collateral exceeds the outstanding debt, ensuring sufficient protection for investors.

Why is the OC test important?

It protects senior debt investors by ensuring there is enough collateral to cover their exposure.

What is a CLO OC trigger?

A CLO OC trigger is the minimum required coverage ratio. If the OC ratio falls below this threshold, the test fails.

What happens when the OC test fails?

Cash flows that would normally go to junior tranches or equity are diverted to repay senior debt.

How often are OC tests calculated?

OC tests are typically calculated monthly and reported in trustee and investor reports.

Conclusion

The CLO overcollateralization test is one of the most important structural protections in CLO deals.

It ensures that the loan collateral backing the transaction remains sufficient to support the issued debt tranches.

For professionals entering the structured finance industry, understanding how the OC test works, how triggers operate, and how breaches affect the waterfall is essential.

Whether you work in trustee reporting, CLO administration, middle office, or deal surveillance, this concept appears frequently in real workflows.

If you want to build strong expertise in structured finance, continue exploring practical learning resources on Structured Finance Academy (SFA).

Mastering these concepts will help you understand deals better, perform confidently in interviews, and grow faster in CLO careers.

Suggested Next Articles