Interest Coverage Test in CLO: A Simple Guide for Professionals

Many professionals working in structured finance deal with CLO waterfalls, reports, and compliance tests daily — yet one concept that often remains unclear is the Interest Coverage Test in CLO.

You may have seen it in trustee reports or compliance sections, but if someone asked you:

“What exactly triggers it, and what happens when it fails?”

Most people hesitate.

And this is exactly where clarity gives you an edge in interviews and real jobs.

What is Interest Coverage Test in CLO

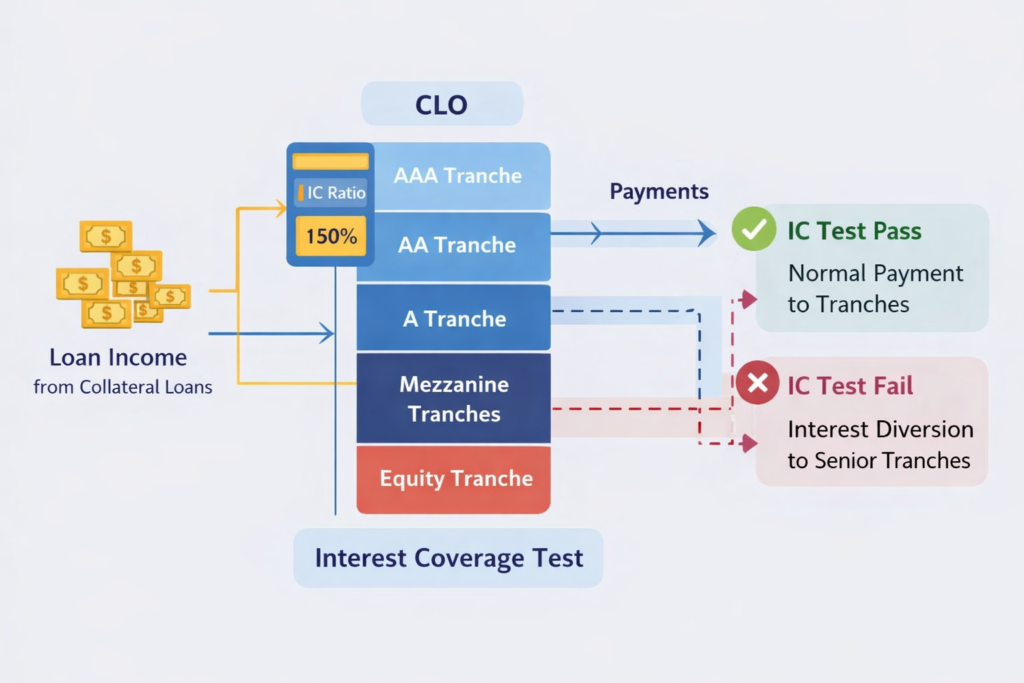

Think of a CLO like a business that earns income (interest from loans) and has to pay expenses (interest to investors).

The Interest Coverage Test in CLO checks:

👉 “Is the income from the loan portfolio enough to pay interest to investors?”

If yes → everything runs smoothly

If no → the deal activates protection mechanisms

Simple Analogy

Imagine:

- You earn ₹1,00,000 per month

- Your EMI obligations = ₹80,000

You’re safe.

But if your income drops to ₹60,000?

You can’t meet obligations → corrective action needed

That’s exactly what the IC test does in a CLO

IC Ratio in CLO Explained

At its core, the test is a ratio:

Interest Coverage Ratio = Interest Income / Interest Payable

The CLO checks this ratio for different tranches.

How It Works Step-by-Step

- Calculate Interest Income

- From underlying loans in the portfolio

- Calculate Interest Due

- For each tranche (AAA, AA, etc.)

- Compute IC Ratio

- Income ÷ Interest obligation

- Compare with Threshold

- Each tranche has a minimum required level

- Determine Pass/Fail

- Above threshold → Pass

- Below threshold → Fail

Example Thresholds

| Tranche | IC Ratio Requirement |

|---|---|

| AAA | 120% – 130% |

| AA | 110% – 120% |

| Mezz | Lower thresholds |

Overcollateralization vs Interest Coverage Test

This is one of the most important distinctions beginners miss.

| Feature | IC Test | OC Test |

|---|---|---|

| Focus | Cash flow (income) | Asset value |

| Measures | Ability to pay interest | Asset backing |

| Trigger type | Income-based stress | Default/valuation stress |

IC Test = Cash flow protection

OC Test = Capital protection

Both work together to protect investors.

Real-World Industry Context

In real structured finance jobs, the Interest Coverage Test in CLO appears everywhere.

Where Analysts Work with IC Test

CLO Middle Office Teams

- Monitor IC ratios monthly

- Flag breaches

- Coordinate with portfolio managers

Trustee Reporting Teams

- Calculate IC ratios

- Include in investor reports

- Validate compliance

Collateral Managers

- Track portfolio income

- Adjust strategy if IC weakens

Investment Banks / Consulting Firms

- Build IC test logic in models

- Perform deal analysis

In reality, this is not just theory — it is part of your daily workflow.

Example: Interest Coverage Test in Action

Let’s simplify with a practical scenario:

CLO Structure

- Loan Portfolio: $500 million

- Average interest income: $30 million/year

Investor Obligations

- AAA interest: $15 million

- AA interest: $8 million

IC Ratio Calculation

For AAA:

IC Ratio = 30 / 15 = 2.0 (200%)

Pass (well above threshold)

Now assume income drops to $18 million:

IC Ratio = 18 / 15 = 1.2 (120%)

Close to threshold → risk zone

If income falls further:

IC Ratio = 14 / 15 = 0.93 (93%)

Fail

What Happens When IC Test Fails?

This is where things get interesting.

CLO activates interest diversion mechanism

Instead of paying lower tranches:

- Cash is redirected to senior tranches

- Junior investors may not receive payments

Where This Appears in Real Workflows

You will encounter IC Test in:

- Trustee reports (monthly/quarterly)

- Investor reporting packages

- Compliance test sections

- Waterfall calculations

- Surveillance dashboards

- Deal monitoring systems

In many roles, your job is:

- Validate IC ratios

- Investigate breaches

- Communicate impact

Common Mistakes or Misunderstandings

Many beginners get confused here:

Thinking IC Test = OC Test

Assuming it measures asset quality (it doesn’t)

Ignoring its link to waterfall

Not understanding trigger consequences

Believing failure means deal collapse (it doesn’t)

Reality:

It is a protective mechanism, not a failure of the deal itself

Why This Concept Matters in CLO Jobs

If you’re working or aspiring to work in:

- Deloitte / EY structured finance teams

- Investment banks

- CLO administrators

- Trustees

- Collateral managers

You WILL encounter this concept regularly.

Practical Importance

- Helps you understand deal health

- Critical for compliance reporting

- Essential for waterfall logic

- Important in investor communication

Knowing this clearly sets you apart from 80% of candidates.

Career Insight: Why Analysts Must Understand This

Understanding the Interest Coverage Test in CLO helps you:

In Interviews

- Answer scenario-based questions

- Explain triggers confidently

In Day-to-Day Work

- Interpret reports better

- Detect issues early

For Career Growth

- Move from execution → understanding

- Gain trust in teams

This is the difference between a data processor and a finance professional

Quick Summary

- IC Test checks if income can cover interest payments

- It is a cash flow-based protection mechanism

- Failure leads to interest diversion

- Used in reporting, compliance, and waterfall

- Critical for structured finance roles

FAQ: Interest Coverage Test in CLO

1. What is Interest Coverage Test in CLO?

It measures whether CLO income is sufficient to pay interest to investors.

2. Why is IC Test important?

It protects senior investors by ensuring they are paid first.

3. What happens when IC test fails?

Cash is diverted from junior tranches to senior tranches.

4. How is IC Ratio calculated?

Interest income divided by interest payable.

5. Is IC Test same as OC Test?

No. IC focuses on income, OC focuses on asset value.

Conclusion

The Interest Coverage Test in CLO is not just a theoretical concept — it is a core mechanism that drives cash flow protection, investor safety, and deal stability.

Once you understand it clearly, you will:

✔ Read CLO reports with confidence

✔ Understand waterfall logic deeply

✔ Perform better in interviews and real roles

If you want to master structured finance, this is one of the foundational concepts you must get right.

Explore more such simplified guides on Structured Finance Academy (SFA) and build real expertise.

Suggested Next Articles

What is a CLO?

CLO Waterfall Explained

Overcollateralization Test in CLO Deals Explained