Most candidates fail to explain this in interviews — but it’s actually simple.

Most people hear the term “waterfall” in finance…

But what does it actually mean?

A waterfall simply refers to how cash or payments are distributed in a specific order.

This concept is used across:

- Loans

- Structured finance

- CLOs

Before we dive into CLO waterfall…In this article, we’ll break down how a CLO waterfall works in a simple, step-by-step way with a diagram and example.

Let’s quickly understand what a “waterfall” means in finance.

A waterfall simply refers to how cash or payments are distributed in a specific order.

This concept is used in:

• Loans

• Structured finance

• Securitization deals

Now, let’s see how it works specifically in a CLO.

Collateralized Loan Obligations (CLOs) can appear complex when you first encounter them. However, once you understand the CLO waterfall, the structure becomes much easier to analyze.

For analysts, especially those preparing for roles in structured finance teams, collateral management firms, trustees, and middle-office operations, understanding the waterfall is essential. In practical terms, the waterfall tells us who gets paid, in what order, and from which cash flows.

This article explains the CLO waterfall in simple language, using a realistic but simplified example inspired by common CLO indenture structures. The goal is to help analysts understand how cash moves through a CLO each payment period.

1. Waterfall payment structure explained

A CLO waterfall is the priority of payments that determines how cash generated by the CLO’s loan portfolio is distributed.

The waterfall is documented in the Indenture, which is the legal document governing the CLO transaction.

Every payment period (usually quarterly or monthly), the CLO collects:

- Interest from underlying leveraged loans

- Principal repayments or loan prepayments

- Fees and expenses

These cash flows are then distributed according to a strict priority structure.

Think of the waterfall as a series of buckets arranged from top to bottom.

- The top bucket gets filled first.

- Only after it is full does cash move to the next bucket.

2. Two Types of CLO Waterfalls

Most CLOs have two main waterfalls:

1. Interest Waterfall

Used to distribute interest income generated by the loan portfolio.

Payments typically include:

- Trustee and administrative fees

- Senior management fees

- Interest payments to CLO debt tranches

- Subordinated management fees

- Equity distributions

2. Principal Waterfall

Used to distribute principal collections such as:

- Loan repayments

- Prepayments

- Sale proceeds

Principal cash is primarily used to:

- Reinvest in new loans during the reinvestment period

- Pay down CLO notes if tests fail

- Redeem debt tranches sequentially

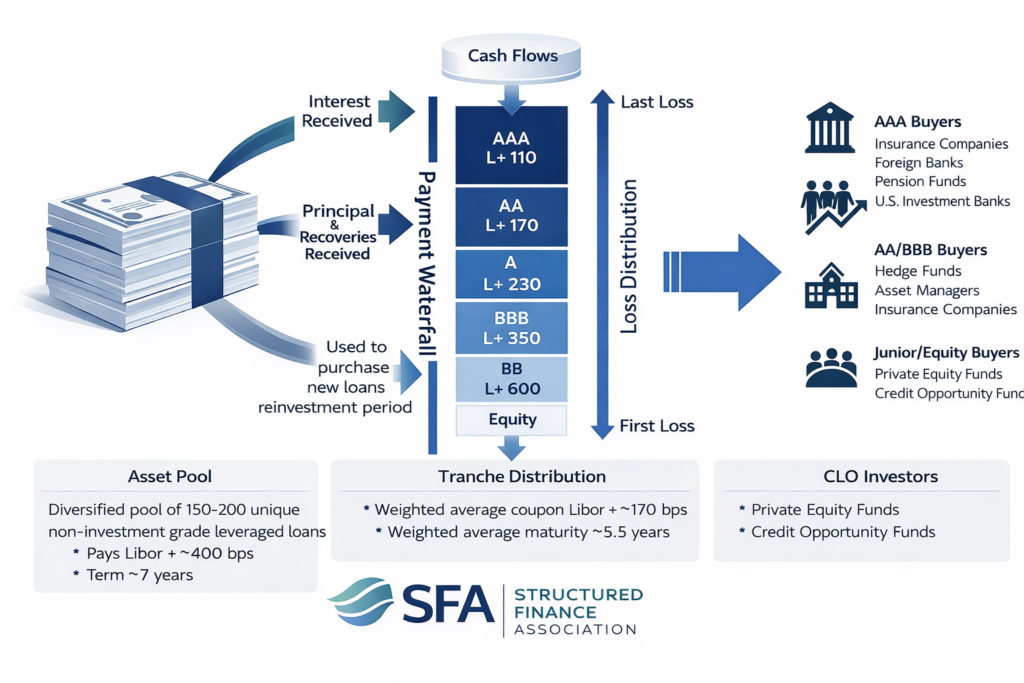

3. Typical CLO Capital Structure

Before understanding the waterfall, analysts should understand the CLO liability structure.

A simplified CLO might look like this:

| Tranche | Rating | Size | Coupon |

|---|---|---|---|

| Class A | AAA | $300M | SOFR + 1.50% |

| Class B | AA | $50M | SOFR + 2.20% |

| Class C | A | $30M | SOFR + 3.00% |

| Class D | BBB | $20M | SOFR + 4.50% |

| Subordinated Notes | Equity | $50M | Residual |

Total CLO Size = $450M

The CLO then invests in approximately $450M of leveraged loans.

4. Simplified Interest Waterfall

Below is a simplified example inspired by the typical payment priority seen in CLO indentures.

Step-by-Step Interest Waterfall

During each payment date, interest proceeds are generally distributed in the following order:

1. Trustee and Administrative Fees

These include payments to:

- Trustee

- Collateral administrator

- Paying agent

Example:

- Trustee fee = $50,000

2. Senior Management Fee

Paid to the collateral manager for managing the portfolio.

Example:

- 0.15% of collateral balance annually

3. Interest on Class A Notes

The most senior debt tranche.

Example:

- Class A outstanding = $300M

- Coupon = SOFR + 1.50%

If SOFR = 5%

Interest due:

$300M × 6.5% / 4 = $4.875M quarterly

4. Interest on Class B Notes

Next tranche receives payment.

Example:

- $50M outstanding

- Coupon = SOFR + 2.20%

Quarterly payment:

$50M × 7.2% / 4 = $0.90M

5. Interest on Class C Notes

Next level of risk.

6. Interest on Class D Notes

Lower-rated tranche.

7. Subordinated Management Fee

Some CLOs include additional manager compensation here.

Example:

- 0.35% annually

8. Equity Distribution

Whatever cash remains flows to equity investors.

This is why CLO equity can generate high returns if the loan portfolio performs well.

5. Simple Numerical Example

Let’s assume the CLO portfolio generates:

Total Interest Collected This Quarter = $8 million

Now distribute according to the waterfall.

Step 1 – Fees

Trustee + admin fees = $0.1M

Remaining cash:

$8M – $0.1M = $7.9M

Step 2 – Senior Management Fee

Manager fee = $0.2M

Remaining:

$7.9M – $0.2M = $7.7M

Step 3 – Class A Interest

Payment required = $4.875M

Remaining:

$7.7M – $4.875M = $2.825M

Step 4 – Class B Interest

Payment required = $0.90M

Remaining:

$2.825M – $0.90M = $1.925M

Step 5 – Class C Interest

Payment required = $0.60M

Remaining:

$1.925M – $0.60M = $1.325M

Step 6 – Class D Interest

Payment required = $0.40M

Remaining:

$1.325M – $0.40M = $0.925M

Step 7 – Subordinated Management Fee

Manager receives additional $0.15M.

Remaining:

$0.925M – $0.15M = $0.775M

Step 8 – Equity Distribution

Remaining amount distributed to equity investors.

Equity cash flow = $775,000

6. What Happens When Tests Fail?

CLO waterfalls are not static.

They can change depending on coverage tests.

Two important tests are:

Overcollateralization (OC) Test

Ensures the loan portfolio provides enough collateral relative to debt.

Example:

Required OC ratio for Class A = 120%

If the ratio falls below the threshold, the waterfall diverts cash away from equity.

Instead, the cash is used to pay down senior notes.

Interest Coverage (IC) Test

Measures whether portfolio interest income covers debt interest obligations.

Example:

Required IC ratio = 150%

If the test fails:

- Equity distributions stop

- Cash is redirected to senior note repayment

7. Principal Waterfall Explained

Principal collections include:

- Loan repayments

- Prepayments

- Loan sales

How this cash is used depends on the reinvestment period.

During Reinvestment Period

Principal proceeds are usually reinvested into new loans.

Example:

Loan repayment = $10M

Manager purchases:

- New leveraged loan

- Price = 99

Principal continues generating interest income.

After Reinvestment Period

Principal proceeds are used to pay down CLO notes sequentially.

Typical order:

- Class A redemption

- Class B redemption

- Class C redemption

- Class D redemption

- Equity receives residual

This is called sequential amortization.

8. Role of the Trustee and Collateral Manager

In practice, the waterfall is operationally executed by multiple parties.

Collateral Manager

Responsible for:

- Managing loan portfolio

- Trading loans

- Monitoring portfolio tests

Examples of global managers include large asset managers specializing in leveraged loans.

Trustee

The trustee performs several operational tasks:

- Calculates waterfall payments

- Maintains noteholder records

- Ensures compliance with indenture rules

- Distributes payments

Trustees rely heavily on cash flow models and reporting systems.

9. Why Analysts Must Understand the Waterfall

In real CLO operations, analysts frequently work with:

- Payment date reports

- Waterfall models

- Trustee reports

- Compliance tests

Typical analyst tasks include:

- Validating interest proceeds

- Reconciling tranche interest calculations

- Monitoring OC/IC tests

- Reviewing trustee payment files

- Checking portfolio cash flows

Understanding the waterfall helps analysts answer questions like:

- Why did equity receive less cash this quarter?

- Why were senior notes partially redeemed?

- Why did reinvestment stop?

10. Common Mistakes Analysts Make

When learning CLO waterfalls, analysts often misunderstand:

Mixing Interest and Principal Waterfalls

These are separate streams.

Interest usually funds debt coupons, while principal funds reinvestment or amortization.

Ignoring Coverage Tests

Coverage tests can redirect cash flows, changing expected distributions.

Misinterpreting Equity Returns

Equity returns depend on:

- Loan spreads

- Default rates

- Trading gains

- Fees

11. Key Takeaway

The CLO waterfall is the core engine of a CLO transaction.

It determines how cash generated by leveraged loans flows through the structure.

In simplified terms:

Loans generate cash → Cash enters waterfall → Payments follow strict priority

Senior investors are protected through:

- Priority payments

- Overcollateralization tests

- Interest coverage tests

Equity investors receive residual returns, but they also bear the highest risk.

For analysts working with CLOs, mastering the waterfall is critical because it connects:

- Loan portfolio performance

- Debt tranche payments

- Equity distributions

Once you understand the waterfall mechanics, the entire CLO structure becomes far easier to analyze. [know more about CLO Structures]

GENERAL WATERFALL vs CLO WATERFALL

Waterfall is a general concept in finance.

But in CLOs:

• It is more structured

• It involves multiple tranches

• It is linked to credit risk

This is why CLO waterfalls are more complex than basic loan waterfalls.

Tip for Job Aspirants

When preparing for structured finance interviews, you should be able to explain:

- CLO capital structure

- Interest vs principal waterfall

- OC and IC tests

- Reinvestment period mechanics

If you can clearly explain the waterfall with a numerical example, interviewers will know you understand CLO cash flow mechanics.

FINAL FAQ SECTION

What is a waterfall in finance?

A waterfall in finance refers to the order in which cash flows or payments are distributed among different stakeholders.

Instead of payments being made randomly, they follow a predefined priority structure, where some investors or obligations are paid before others.

This concept is widely used in:

- Loans

- Structured finance

- Securitization deals

What is a CLO waterfall?

A CLO (Collateralized Loan Obligation) waterfall is the payment structure that determines how cash generated from a pool of loans is distributed among different investors.

In a CLO:

- Payments are made in a strict sequence

- Senior debt investors are paid first

- Equity investors are paid last

This structure ensures risk is allocated properly across different tranches.

Who gets paid first in a CLO?

In a CLO waterfall, payments follow a strict hierarchy:

- Fees and expenses

- Senior (AAA) tranche investors

- Mezzanine tranche investors

- Equity investors (last)

Senior investors are paid first because they take lowest risk, while equity investors receive residual cash and bear the highest risk.

How does CLO cash flow work?

CLO cash flow comes from the interest and principal payments made by underlying loans.

This cash is then distributed through the waterfall:

→ First, operational fees are paid

→ Then, senior investors receive payments

→ Followed by mezzanine investors

→ Any remaining cash goes to equity holders

If cash flows decline, equity investors are impacted first, while senior investors remain protected.

Suggested next reading–