CLO warehousing phase is where a future CLO quietly begins taking shape long before investors ever see the final transaction. Behind the scenes, CLO managers are actively acquiring syndicated loans, negotiating secondary market trades, managing warehouse financing costs, monitoring portfolio concentrations, and navigating settlement mechanics like assignments and participations. Millions of dollars of leveraged loan exposure may move daily during this period, making warehousing one of the most operationally intense and risk-sensitive phases in the entire CLO lifecycle. Yet, despite its importance, many professionals entering structured finance only see the final CLO structure — not the complex accumulation process happening underneath.

Many professionals hear terms like:

- warehouse lines,

- ramp-up,

- syndicated loans,

- assignments,

- participations,

- secondary loan trading,

- and CLO collateral accumulation,

but very few truly understand what actually happens before a CLO officially closes.

And this is where things become interesting.

Before a billion-dollar CLO is launched, there is often a silent but extremely high-pressure phase happening behind the scenes.

Loans are being sourced.

Banks are syndicating exposure.

CLO managers are racing against market volatility.

Traders are negotiating prices.

Settlement teams are processing assignments and participations.

And millions of dollars of exposure may be moving daily across the secondary loan market.

In this article, we simplify the warehousing phase using practical examples, numbers, and real-world style scenarios.

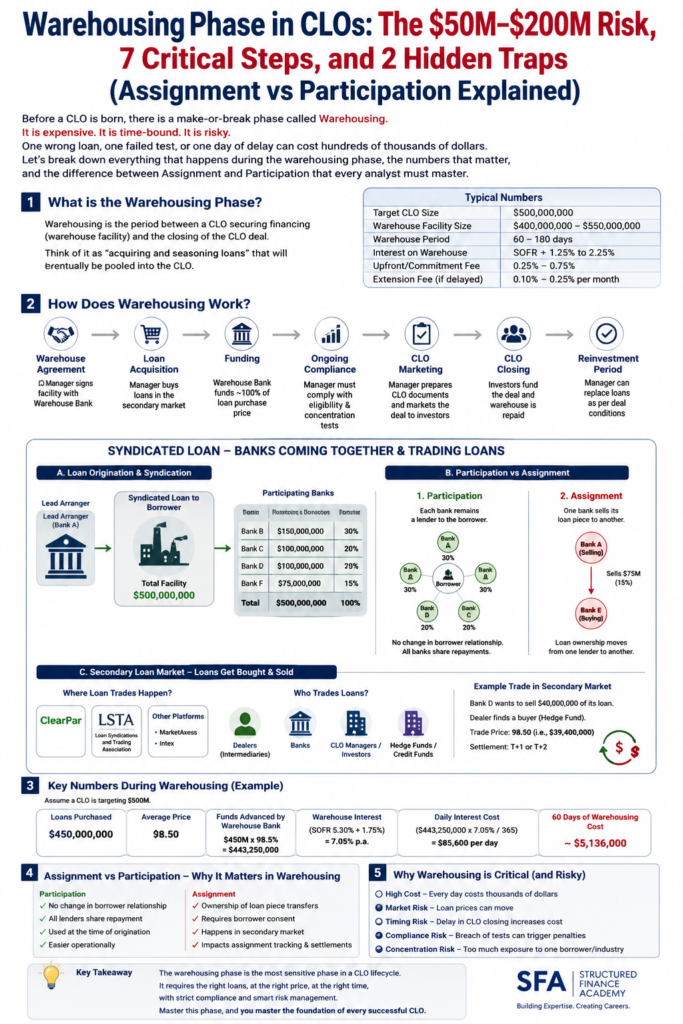

What Is the CLO Warehousing Phase?

Imagine a CLO manager wants to launch a:

$600 million CLO.

But there is a problem.

The manager cannot suddenly buy $600 million of loans on the closing date.

Instead, the manager gradually accumulates loans over several weeks or months before the CLO issuance.

This pre-CLO accumulation period is called the:

Warehousing Phase.

The loans are temporarily financed using a warehouse facility provided by banks.

Example: How a CLO Warehouse Actually Works

Suppose:

Target CLO Size

$600 million

Equity Contribution

$60 million

Warehouse Financing

$540 million

The CLO manager now starts purchasing syndicated loans.

| Loan Type | Purchase Amount |

| Telecom Loan | $120 million |

| Healthcare Loan | $90 million |

| Software Loan | $140 million |

| Infrastructure Loan | $110 million |

| Energy Loan | $80 million |

| Consumer Loan | $60 million |

Over time, the warehouse slowly builds the future CLO portfolio.

This phase is extremely important because the quality of warehouse collateral can significantly impact the future performance of the CLO.

1. The CLO Manager Starts Hunting for Loans

This is where syndicated loans become critical.

Large companies may require:

- $1 billion,

- $3 billion,

- or even $10 billion financing.

One bank usually does not take the entire exposure.

Instead, multiple banks come together through:

Loan Syndication.

Example:

| Bank | Commitment |

| Bank A | $1.5 billion |

| Bank B | $1 billion |

| Bank C | $750 million |

| Bank D | $750 million |

Once these loans enter the market, CLO managers may start purchasing pieces of those loans for the warehouse.

2. Loans Are Bought in the Secondary Market

This surprises many beginners.

A CLO manager does not always buy loans directly from the original syndication.

Many loans are purchased in the:

Secondary Loan Market.

This means:

- banks,

- CLOs,

- hedge funds,

- mutual funds,

- and institutional investors

actively buy and sell loan exposure.

Example of Secondary Trading

Suppose a bank wants to reduce exposure to a telecom borrower.

The bank sells:

$25 million loan exposure

at:

Price = 98

The CLO manager buys the position.

Total purchase cost:

$24.5 million

If the loan later trades at:

101

the unrealized gain becomes:

$750,000.

This active trading activity is one reason why the warehouse phase becomes operationally intense.

3. Assignment Trades Start Flowing Through Operations Teams

One of the biggest hidden operational areas during warehousing is:

Loan Settlement.

Many warehouse purchases settle through:

Assignments

In an assignment:

- ownership transfers,

- lender of record changes,

- buyer gets direct borrower rights.

Example:

Bank A sells:

$15 million Software Loan

to a CLO manager.

After settlement:

- CLO becomes lender of record,

- administrative agent updates records,

- future payments flow directly to CLO.

This process may involve:

- trade confirmations,

- borrower consents,

- administrative agents,

- delayed compensation calculations,

- and settlement platforms.

4. Participation Trades Also Increase During Warehousing

Not every trade settles as an assignment.

Sometimes trades occur through:

Participations

In participation:

- original lender remains lender of record,

- economic exposure transfers,

- participant does not directly face borrower.

Example:

Bank A participates:

$10 million Healthcare Loan

to Fund B.

Borrower still recognizes Bank A.

But economic benefits move to Fund B.

This structure may be used when:

- borrower consent is difficult,

- timing becomes critical,

- or settlement flexibility is needed.

5. Warehouse Risk Starts Building Quietly

This is one of the most dangerous phases.

Why?

Because the CLO is not yet fully priced.

Suppose the manager buys loans at:

99.5

But market volatility suddenly pushes loan prices to:

On a:

$400 million warehouse portfolio,

that can create a mark-to-market decline of:

$18 million.

This is why warehouse management requires:

- credit analysis,

- diversification monitoring,

- spread management,

- and market awareness.

6. Diversification Becomes Extremely Important

During warehousing, managers cannot simply buy random loans.

They need to monitor:

- industry concentrations,

- borrower exposure,

- ratings mix,

- spread profile,

- WARF,

- and portfolio quality.

Example:

If too much exposure builds toward:

- healthcare,

- telecom,

- or energy,

future CLO tests may become difficult.

This is why warehouse portfolio construction becomes both:

- an investment challenge,

- and a compliance challenge.

7. The Warehouse Eventually Becomes the CLO

Once enough collateral is accumulated:

the warehouse transitions into the final CLO.

The loans accumulated during warehousing become collateral backing different CLO tranches.

Example:

| Tranche | Amount |

| AAA | $350 million |

| AA | $80 million |

| A | $50 million |

| BBB | $40 million |

| BB | $20 million |

| Equity | $60 million |

From this point onward:

cash flows start moving through the CLO waterfall.

Why Understanding Warehousing Can Transform Your Career

Many professionals only learn isolated operational processes.

But understanding the warehousing phase helps connect:

- syndicated lending,

- secondary loan trading,

- settlements,

- assignments,

- participations,

- collateral management,

- and CLO structuring.

That broader understanding can open opportunities in:

- CLO Operations,

- Loan Settlements,

- Middle Office,

- Trade Support,

- Portfolio Administration,

- Trustee Services,

- Structured Credit Analytics,

- and Warehouse Financing Teams.

Final Thoughts

The warehousing phase is where a CLO quietly takes shape long before investors ever see the final transaction.

It is a phase filled with:

- loan accumulation,

- market risk,

- secondary trading,

- assignments,

- participations,

- operational coordination,

- and portfolio construction decisions.

For beginners, this ecosystem may initially look complex.

But once you understand how warehouse financing, syndicated loans, and secondary loan trades connect together, the broader CLO market becomes far easier to understand.

And for professionals entering structured finance, mastering the CLO Warehousing Phase Explained may become one of the strongest differentiators in long-term career growth.

Assignment vs Participation: Why Some Loan Trades Transfer Ownership While Others Don’t

One of the most misunderstood areas in the syndicated loan market is the difference between Assignments and Participations.

At first glance, both seem similar.

In both cases:

- a lender reduces exposure,

- another party gains economic exposure,

- and a loan position changes hands.

But operationally and legally, they are very different.

And understanding this difference becomes extremely important during:

- CLO warehousing,

- secondary loan trading,

- settlements,

- and portfolio management.

What Is an Assignment?

In an Assignment, the loan ownership actually transfers from the seller to the buyer.

Example:

Bank A sells:

$20 million of a syndicated loan

to:

CLO Fund B.

After settlement:

✅ CLO Fund B becomes the new lender of record

✅ Administrative agent updates lender register

✅ Interest and principal payments go directly to Fund B

✅ Fund B gains direct rights against the borrower

This is why assignments are often considered a “true transfer” of the loan exposure.

Why Assignments Are Often Preferred

Assignments are generally preferred because they provide:

✅ Direct borrower relationship

✅ Legal ownership transfer

✅ Stronger lender protections

✅ Cleaner settlement structure

✅ Better transparency for portfolio tracking

For CLOs and institutional investors, assignments are usually operationally cleaner because the buyer directly owns the loan exposure.

This becomes especially important for:

- voting rights,

- amendments,

- restructurings,

- and workout situations.

Then Why Use Participations?

Because assignments are not always easy.

Some assignments may require:

- borrower consent,

- agent approval,

- extensive documentation,

- or longer settlement timelines.

During volatile markets or tight warehouse timelines, waiting too long can become expensive.

This is where Participations become useful.

What Is a Participation?

In a participation:

❌ Legal ownership does NOT transfer

❌ Original lender remains lender of record

Instead:

✅ Economic exposure transfers

Example:

Bank A participates:

$15 million exposure

to:

Fund B.

Borrower still officially recognizes Bank A.

But Bank A passes economic payments to Fund B.

Why Participations Are Used

Participations may be preferred when:

✅ Speed matters

✅ Borrower consent is difficult

✅ Confidentiality is important

✅ Temporary exposure transfer is needed

✅ Settlement flexibility is required

They can sometimes help market participants move risk faster during warehousing or active trading periods.

The Hidden Trade-Off

Participations create an additional layer of dependency.

Because:

Fund B does not directly face the borrower.

Instead, Fund B relies on:

Bank A.

So if operational issues arise, participation structures may become more complex than assignments.

Simple Analogy

Assignment:

“Selling the house.”

Participation:

“Sharing the rental income without changing ownership.”

Why This Matters in CLOs

During the CLO warehousing phase, managers actively acquire loans from the secondary market.

Understanding whether exposure settles through:

- assignments,

- or participations,

can impact:

- timing,

- compliance,

- operational workflows,

- borrower rights,

- and warehouse risk management.

And this is one reason why experienced CLO professionals often develop strong knowledge of:

- syndicated loans,

- settlement mechanics,

- and secondary market structures.

Because in structured finance, operational understanding can become a major career differentiator.

Further Readings…